[This post is an excerpt from a recent TSI commentary]

There are three reasons that the Trump Presidency will very likely go down in history as a disaster for the US, only the last of which has anything to do with Trump. The first two reasons are inter-related in that they are primarily the consequences of distortions/imbalances created by the Federal Reserve.

Due largely to the aggressive interventions of the Fed, including the creation of trillions of dollars via QE programs and keeping interest rates pegged near zero for eight years, the mal-investment problem in the US economy today is more serious than the mal-investment problem that led to the “great recession” of 2007-2009. This means that the next recession will probably be even more severe than the previous episode. It is possible that the extension of ultra-easy monetary conditions combined with fiscal ‘stimulus’ in the form of tax cuts will delay the start of the next recession by another 6-12 months, but for no fault of Trump it will almost certainly happen on his watch.

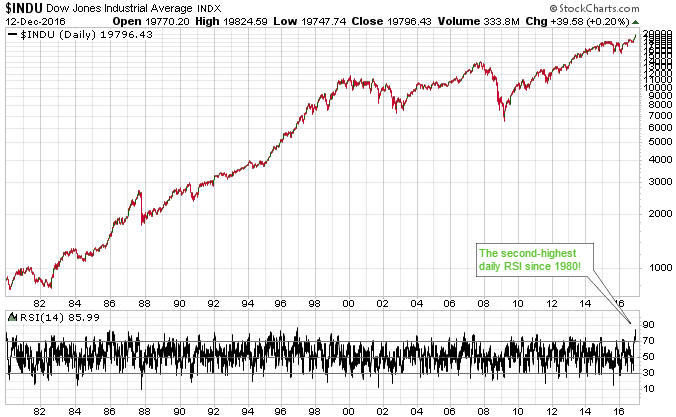

Also due to the aggressive interventions of the Fed, the US stock, bond and real-estate markets are now valued at levels that all but guarantee terrible performance over the coming few years. As is the case with an economic recession, it is possible that the extension of ultra-easy monetary conditions combined with fiscal ‘stimulus’ in the form of tax cuts will delay the start of the coming period of terrible performance; however, for no fault of Trump there will very likely be bear markets in the major US asset classes during his first — and almost certainly only — Presidential term.

While the coming severe recession and the bearish trends in asset prices were bound to occur and clearly have nothing to do with Trump, it looks like Trump is unwittingly setting himself up to take the blame.

His one chance of avoiding blame and paving the way for a genuine recovery to be in progress by the time of the next Presidential election would have been to stay out of the way and allow a major liquidation of the mal-investments to happen during the first half of 2017. This would have enabled the blame for the debacle to be appropriately placed at the feet of the Fed and the preceding Administration. However, having previously (and correctly) chided the Fed for having created a “big, fat, ugly bubble”, it seems that the deadly combination of hubris and ignorance has convinced Trump that he can set in motion a long period of strong growth with no intervening painful purgation.

In summary, certain bad economic and financial-market outcomes are currently set in stone. What’s not set in stone is who gets the blame. Unfortunately, Trump appears to be positioning himself to take the blame for the economic damage caused by others.