[This blog post is an excerpt from a commentary published at speculative-investor.com about one week ago]

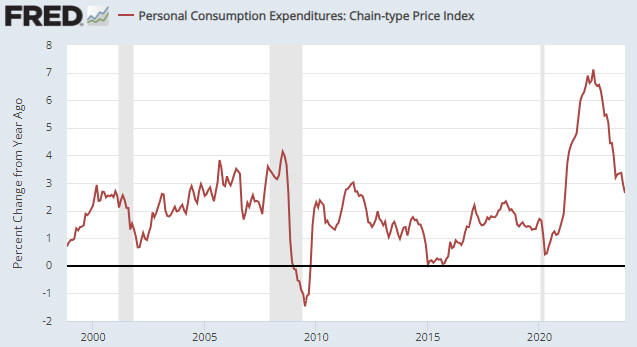

The latest calculation of the Personal Consumption Expenditures (PCE) Index, an indicator of “inflation”, was reported on Friday morning (22nd December) in the US. The following chart shows that the latest number extended the downward trend in the index’s year-over-year (YOY) growth rate, which is now 2.6%. Moreover, the “core” version of the PCE Index, which apparently is the Fed’s favourite inflation gauge, has risen at an annualised rate of only 1.9% over the past six months. This essentially means that the Fed’s inflation target has been reached. What does this mean for the financial markets?

An implication of the on-going downward trends in popular indicators of inflation is that the Fed will slash its targeted interest rates next year. That’s a large part of the reason why the stock and bond markets have been celebrating over the past two months.

It’s important to understand, however, that the markets already have priced in a decline in the Fed Funds Rate (FFR) from 5.50% to 3.75% (the equivalent of seven 0.25% rate cuts). This means that for the rate-cut celebrations to continue, the financial world will have to find a reason to price in more than seven rate cuts for next year. Not only that, but for the rate-cut celebrations to continue in the stock market the financial world will have to find a reason to price in more than seven 2024 rate cuts while also finding a reason to price in sufficient economic strength to enable double-digit corporate earnings growth during 2024. That’s a tall order, to put it mildly.

Our view is that the Fed will end up cutting the FFR to around 2.0% by the end of next year, meaning that we are expecting about twice as much rate cutting as the markets currently have priced in. The thing is, our view is predicated on the US economy entering recession within the next few months, and Fed rate-cutting in response to emerging evidence of recession has never been bullish for the stock market. On the contrary, the largest stock market declines tend to occur while the Fed is cutting its targeted rates in reaction to signs of economic recession.

Fed rate cuts in response to emerging evidence of recession are, however, usually bullish for Treasury securities and gold. That’s why we expect the upward trends in the Treasury and gold markets to continue for many more months, with, of course, corrections along the way.