To know whether or not the Fed has been a long-term success, the reason for the Fed’s creation must first be known. Here is the reason from the horse’s mouth: “It [the Fed] was created by the Congress to provide the nation with a safer, more flexible, and more stable monetary and financial system.” If this is the real reason then over the long-term the Fed has not been a success. In fact, it has been an abject failure.

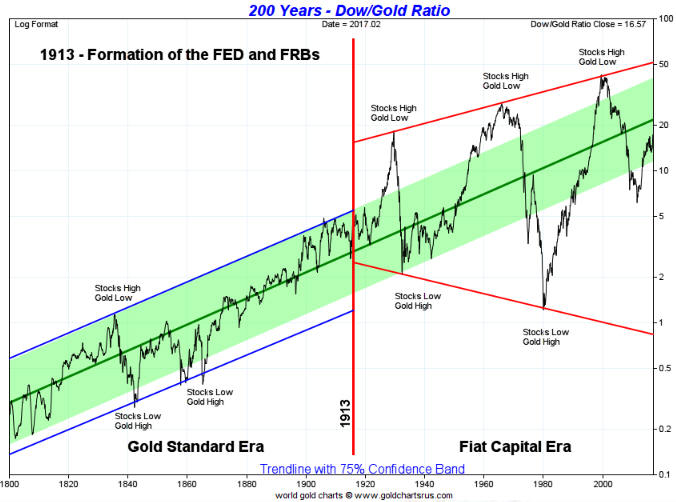

That the Fed has blatantly not been successful in providing the nation with a more stable monetary and financial system is clearly evidenced by the following ultra-long-term chart from www.goldchartsrus.com. This chart shows that the Dow/gold ratio experienced much greater long-term volatility post-Fed than it did pre-Fed.

This doesn’t mean that the Fed hasn’t been a success, only that it hasn’t been a success if judged based on its publicly-stated purpose.

If the Fed was actually created to ensure that the government could borrow and spend with no rigid limit and to enable the banking industry to grow its collective balance sheet far beyond what would be possible under a less ‘flexible’ monetary system, then the Fed has been a resounding success.