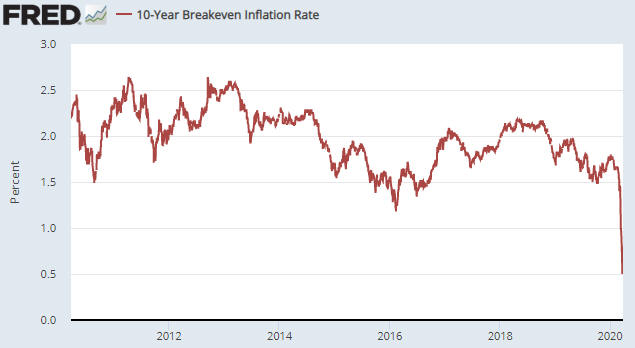

Inflation expectations have crashed along with the stock market and the oil price. This is evidenced by the following chart of the 10-Year Breakeven Inflation Rate, which indicates the average CPI that the market expects the government to report over the years ahead. Since the advent of the TIPS (Treasury Inflation Protected Securities) market in 2003, the Expected CPI was only below last Friday’s level of 0.50% during November-December of 2008 and January of 2009, that is, during the concluding months of the Global Financial Crisis.

The collapse in inflation expectations over the past several weeks does not indicate that “inflation” will be much lower in the future. On the contrary, beyond the short-term it greatly increases the risk of higher “inflation”.

Over the next few months the CPI will be lower than would have been the case in the absence of the coronavirus-related restrictions to economic activity and the plunge in the oil price, but by this time next year the CPI probably will be much higher due to the following:

1) Aggressive central bank reactions to the economic slowdown and the stock market plunge. These reactions will distort prices and hamper the economy, but to a man with nothing except a hammer every problem looks like a nail. To a central banker, every economic problem other than obvious “price inflation” looks like a reason to create more money and credit out of nothing. Also, to the central bankers of the world the recent rapid decline in inflation expectations is like a giant cattle prod pushing them in the direction of pro-inflation monetary policy.

2) In addition to aggressive monetary stimulus there will be aggressive fiscal stimulus. This would be the case anyway under such circumstances, but in the US the short-term stimulus from increased government spending will be more aggressive than usual due to this being an election year.

3) Once the coronavirus threat dissipates, there will be the natural release of pent-up demand.

4) The widespread shutting down of mines, production facilities and trade-related transportation will damage supply chains, in some cases permanently due to parts of ‘chain’ going bust, and ensure that it will take more time than usual for producers to respond to increased demand and rising prices.

Adding the natural force of pent-up demand release to the unnatural forces of monetary/fiscal stimulus and supply disruptions resulting from forced shut-downs should mean that “inflation” will be materially higher a year from now than would have been the case in the absence of the Q1-2020 calamity. My prediction: During the first half of 2021 the official US CPI, which routinely understates the increase in the cost of living, will print above 4%.