[This blog post is an excerpt from a TSI commentary published on 5th June 2022]

A point we’ve made many times in the past* is that gold and the world’s most important equity index (the S&P500 Index – SPX) are at opposite ends of a virtual investment seesaw. Due to their respective natures, if one is in a long-term bull market then the other must be in a long-term bear market. In multi-year periods when they are both trending upward in dollar terms it means that the dollar is in a powerful bear market, not that gold and the SPX are simultaneously in bull markets (the one that is actually in a bull market will be determined by the performance of the gold/SPX ratio). Recently, our ‘investment seesaw’ concept was part of the inspiration for the Synchronous Equity and Gold Price Model (SEGPM) created by Dietmar Knoll. This model is a quantitative relationship between the SPX, the US$ gold price and the US money supply (the model uses the M2 monetary aggregate), and is explained on pages 251-266 of Incrementum’s latest “In Gold We Trust” report.

Before delving into how the SEGPM works, it’s worth pointing out that there have been previous attempts to link changes in the stock market and the gold price to changes in the money supply. These attempts failed. With regard to the stock market they failed because a strong positive correlation between the senior equity index and the money supply only exists during equity bull markets, that is, the money supply in isolation fails to account for the major swings in the stock market. For example, during the 9-year period from March-2000 to March-2009 there was huge growth in the US money supply, but the SPX was 50% lower at the end than it was at the start of this period.

With regard to the gold market the aforementioned attempts failed first and foremost because the underlying premise is wrong, in that there is no good reason for the gold price to track the US money supply. Also, we know from the historical record that valuations for gold that are based solely on the US money supply can deviate hugely from the real world for DECADES at a time, which means that they have no practical value.

The sorts of models mentioned above have never worked over complete cycles because they consider the SPX and the money supply or gold and the money supply, as opposed to an SPX-gold combination (both ends of the ‘investment seesaw’) and the money supply.

The SEGPM is based on the idea that there are periods when an increase in the money supply will boost the SPX more than it will boost the gold price and other periods when an increase in the money supply will boost the gold price more than it will boost the SPX, with the general level of trust/confidence** in money, the financial system and government determining whether the SPX or gold is the primary beneficiary of monetary inflation. During long periods when trust/confidence is high or trending upward, increases in the money supply will tend to do a lot for the SPX and very little for gold. The opposite is the case during long periods when trust/confidence is low or falling.

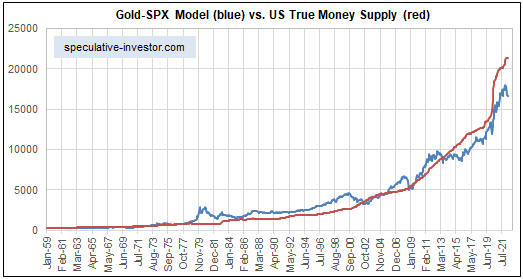

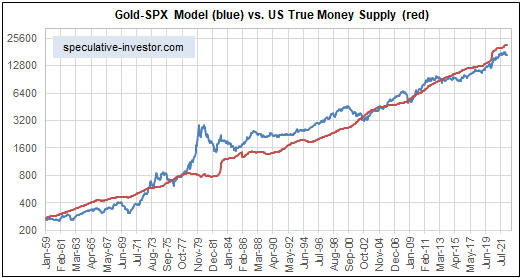

Dietmar Knoll found that adding the SPX to 1.5-times the US$ gold price (and applying a scaling factor) resulted in a number that has done a good job of tracking the M2 money supply over many decades. The correlation is illustrated by charts included in the above-linked Incrementum report, but we have created our own charts using True Money Supply (TMS) instead of M2. Our charts are displayed below.

Each of the following two monthly charts compares the US TMS with the sum of the S&P500 Index and 1.5-times the US$ gold price. The only difference between these charts is the scaling of the Y-axis. The first chart uses a linear scale and the second chart uses a log scale.

The log-scaled chart displayed above indicates that since 1959 there have been only three multi-year periods during which the SEGPM deviated by a substantial amount from the money supply. The first was during 1969-1971 due to the extreme under-valuation of gold (the gold price was fixed at the time and unable to respond to the monetary inflation and declining confidence of the time). The second was during 1979-1980 due to a gold market bubble. The third was during the second half of the 1990s due to a stock market bubble.

Interestingly, both charts indicate that the current SPX+gold level is low relative to the money supply. If we are right to think that an economic bust (a 1-3 year period of declining confidence) has begun, then this suggests that there is a lot of scope for the gold price to increase over the next couple of years even if the pace of money-supply growth is slow. To be more specific, it suggests the potential for the US$ gold price to double over the next two years with TMS growth of only 5% per year.

*For example, in the May-2017 blog post linked HERE

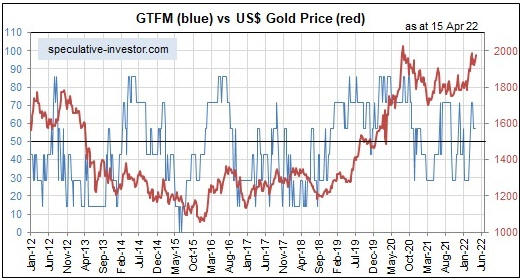

**The general level of trust/confidence is quantified by our Gold True Fundamentals Model (GTFM)

Print This Post

Print This Post