[This is a brief excerpt from a commentary posted at TSI last week]

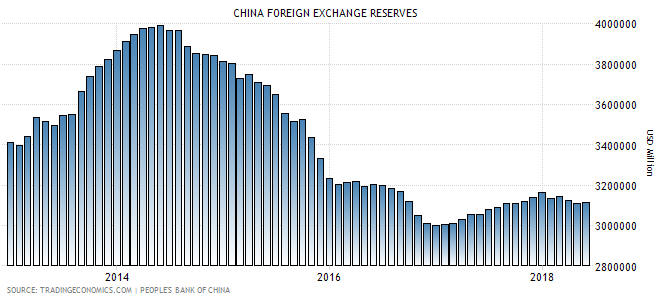

In the 2nd July Weekly Update we discussed the risk posed by the recent weakening of China’s currency (the Yuan), and commented: “We won’t know for sure until China’s central bank publishes its international currency reserve figure for June, but the recent weakening of the Yuan does not appear to be the result of a deliberate move by China’s government.” We now know for sure — the Yuan’s pronounced weakness during the month of June was NOT the result of government manipulation. In fact, it can be more aptly described as the result of an absence of manipulation.

We know that this is so because of what happened to China’s currency reserves in June. As indicated by the final column on the following chart, almost nothing happened (there was no significant change). This means that China’s government made no attempt to either strengthen or weaken its currency last month.

To further explain, for China’s government to engineer weakness in the Yuan’s foreign exchange value it must add to its international currency reserves by exchanging its own currency (that it creates ‘out of thin air’) for foreign currency. By the same token, for China’s government to increase the Yuan’s relative value it must use its international currency reserves to purchase Yuan. Consequently, periods when China’s currency reserve is increasing are periods when China’s government is attempting to weaken the Yuan and periods when China’s currency reserve is decreasing are periods when China’s government is attempting to strengthen the Yuan.

The above chart therefore tells us that China’s government was trying to weaken the Yuan up to mid-2014 and strengthen the Yuan from mid-2014 until the end of 2016. The chart also seems to indicate that there was a tentative attempt to weaken the Yuan during 2017, but 2017’s gradual increase in China’s foreign currency stash was most likely driven by changing market valuation. We are referring to the fact that because reserves are reported in US dollars and held as debt securities, the reported value of the reserves can be altered by a change in exchange rates or bond prices. In particular, the reported reserve figure will have an upward bias during periods when the US$ is weak relative to other major currencies, as it was throughout 2017.

The bottom line is that China’s government has not yet weaponised the Yuan’s FX value in its economic war with the US government, but it is also not standing in the way when the Yuan weakens in response to market forces.