November 17, 2015

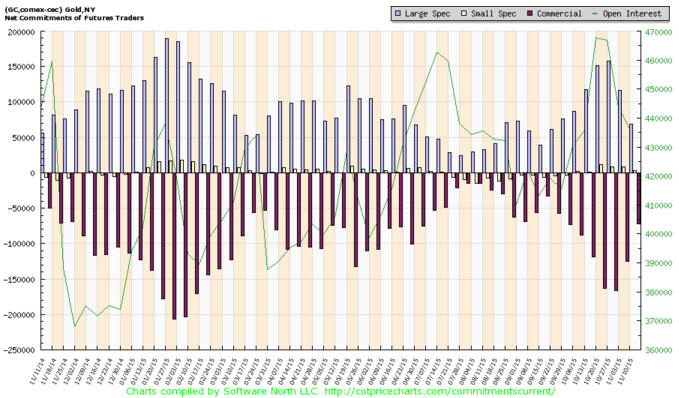

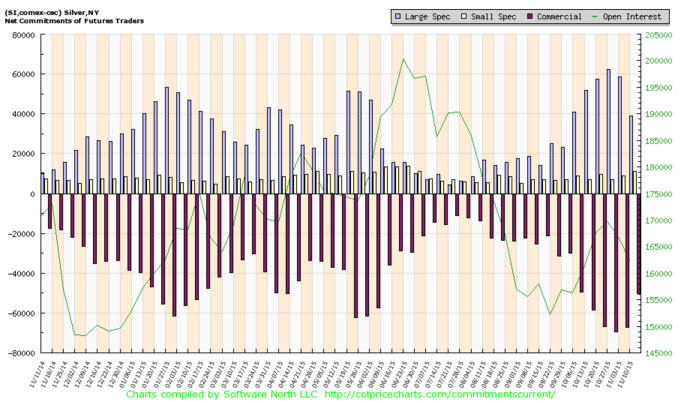

The following charts relate to comments on the gold and silver markets that will be emailed to TSI subscribers later today.

The following charts relate to comments on the gold and silver markets that will be emailed to TSI subscribers later today.

Way back in early-2009 and again in mid-2012 I wrote in TSI commentaries that if the story unfolded as I expected then a lot of future economic commentary would begin with the word “despite”, and that in most cases the commentary would be a lot closer to the truth if “despite” were replaced with “because of”. For example, a comment along the lines of “despite the huge monetary stimulus the economy remains weak” would be closer to the truth if it read “because of the huge monetary stimulus the economy remains weak.”

My 2009 assessment remains applicable in that most commentators still don’t get it and still use “despite” when they should be using “because of”. They still don’t realise that pumping money into the economy falsifies prices (including the price of credit, the most important price of all) in ways that make the economy less, not more, efficient. The reality is that the more the central bank tries to stimulate the economy via ‘loose’ money, the more it will HINDER economic progress.

A sensible way to use the word “despite” is in reference to plans for future stimulus. For example, it could reasonably be said that DESPITE the lack of logical support for creating money out of nothing and the evidence that previous QE programs did not help, it’s a near certainty that the Fed will introduce a new monetisation program if the economy gets much weaker. It could also be said that the US economy’s only hope is that the remnants of capitalism are strong enough to generate sustained improvement DESPITE the price distortions caused by the Fed.

This post is a slightly-modified excerpt from a recent TSI commentary.

The Federal Reserve has monetised a few trillion dollars of bonds over the past seven years without creating much in the way of what most people call “inflation” (a rise in the general price level). How could this happen?

One popular explanation is that the Fed’s Quantitative Easing (QE) adds to bank reserves, but not the economy-wide money supply. According to this line of thinking, the ‘money’ created by the Fed to purchase bonds remains trapped in reserve accounts at the Fed. However, this explanation can be immediately eliminated, because as previously explained every dollar of QE adds one dollar to bank reserves at the Fed AND one dollar to demand deposits within the economy. The fact is that the economy-wide money supply is now a few trillion dollars larger thanks to the Fed’s QE.

A second explanation is that QE isn’t “inflationary” because it involves the exchange of one cash-like instrument for another. This explanation can also be immediately eliminated due to the fact that it mistakenly conflates two very different things — money and debt securities. If you don’t understand the difference, try buying something with a T-Bill. You should then understand. Also, more information on this particular issue can be found in my 9th May post at the TSI Blog.

As an aside, QE is not only NOT an exchange of one cash-like instrument for another, it involves increasing the amount of cash in the financial system and simultaneously decreasing the amount of financial assets that can be bought with cash. That is, it results in more cash ‘chasing’ fewer assets.

A third explanation is that the increase in the money supply stemming from the Fed’s QE has been offset, in terms of effect on the general price level, by a decrease in the velocity of money. This is yet another explanation that can be eliminated, because changes in “money velocity” never explain anything. The reason is that money velocity (V) is nothing more than a fudge factor that makes one side of the tautological and practically-useless equation of exchange (MV = PQ) equal to the other side. It exists in academia, but not in the real world. For more information on the irrelevance of money velocity, refer to my 10th June post at the TSI Blog.

Having eliminated three of the fatally-flawed explanations for why the Fed’s gargantuan QE hasn’t yet led to problematical “price inflation”, I’ll now provide two explanations that make some sense.

First, for decades prior to 2008 almost all of the US economy’s new money was created by commercial banks (commercial banks can loan new money into existence and they can also monetise securities). As a result, the first receivers of the new money tended to be within the ‘general public’ (home buyers/sellers, private businesses, etc.). However, since August-2008 almost two-thirds of all new money has been directly created by the Fed. This means that the first receivers of most of the new money were bond speculators, and that the second, third, fourth and fifth receivers of the new money were probably bond speculators or stock speculators. In other words, rather than being trapped in reserve accounts at the Fed as some people have mistakenly asserted, it is likely that a lot of the new money has effectively been trapped within the financial markets. It will eventually leak out into the ‘real’ economy, but due to the way the money was created/injected there has been a much longer-than-usual delay between the money creation and the inevitable effects on everyday prices.

Second, it’s important to understand that even if it were possible to come up with a single number that reliably reflected the actual change in the economy-wide purchasing-power (PP) of money, this number would not tell us the “inflationary” effect of a change in the money supply. The reason is that to know the effect on money PP of a change in the money supply you have to know what would have happened to PP in the absence of the money-supply change.

For example, let’s assume for the sake of argument that there is a consumer price index (CPI) that reliably indicates the change in the general price level. In our hypothetical example, the CPI would have fallen by 10% over a certain period, but due to money-pumping by the central bank the CPI increases by 2%. In this case the “inflationary” effect of the central bank’s money-pumping is not a 2% increase in the CPI, it is a 12% increase in the CPI (the difference between what happened and what would have happened).

Taking into account the high private-sector debt levels that existed in 2008 and have persisted to this day, it is not hard to imagine that in the absence of the Fed’s money creation there would have been a sizable decline in the CPI rather than a moderate increase. The “inflation” caused by the Fed’s QE is the difference between the decline in the general price level that would have happened and the rise in the general price level that did happen.

In conclusion, there are two main contributors to the lacklustre performance of the “general price level” over the past few years. First, unlike in earlier cycles a lot of the money created during the current cycle was injected directly into the financial markets. Second, it’s likely that there would have been significant “price deflation” in the absence of the money-pumping.

One of the interesting aspects of the financial newsletter business is that an incorrect prediction of a market crash will probably drum-up a lot more new business than a correct prediction that there won’t be a crash. Hence, the never-ending popularity of crash-forecasting, despite the fact that such forecasts almost never pan out.

From the perspective of a newsletter writer or any other commentator on the financial markets, the best thing about forecasting a crash is the massively asymmetric reward-risk associated with it. If the market doesn’t crash this year, when it was supposed to according to your original forecast, then you can just say that the event has been delayed and will happen next year instead. You don’t have much to lose because people will soon forget the failed prediction and focus on the next prediction. And if it doesn’t happen next year, then just repeat the process because eventually the market will crash and your amazing prescience will be there for all to see. Furthermore, after you correctly predict a crash there will be thousands of people eager to find out your next big prediction and buy your newsletter/book. In other words, from the forecaster’s perspective the downside of making an incorrect crash forecast is trivial compared to the upside of making a correct crash forecast.

The point is that regardless of how many times you forecast a crash that never happens, you will only have to get lucky once and you will be set for life. From then on you can promote yourself, and be introduced in interviews, as the person who predicted the great crash of XXXX (insert year). From then on a large herd of ‘investors’ will hang on your every word and rush to buy your advice whenever your next big forecast hits the wires.

Having seen how the process works, I’m officially entering the crash forecasting business. My inaugural forecast is for the US stock market to crash during September-October of 2016.

My forecast isn’t a completely random guess, for four reasons. First, stock-market crashes have a habit of occurring in September-October. Second, the two most likely times for the stock market to crash are during the two months following a bull market peak and in the year after a bull market peak (that is, roughly a year into a new bear market). The 1929 and 1987 crashes are examples of the former, while the 1974 and 2008 crashes are examples of the latter. The current situation is that either 1) a bear market began a few months ago, in which case the opportunity to crash during the two months following the bull market peak was missed and the next opportunity will arrive during the second half of 2016, or 2) the bull market is intact, in which case a major peak is likely during the second half of next year. Third, market valuation is high enough to support an unusually-large price decline. Fourth, interest rates are likely to have an upward bias over the next 12 months.

A few months from now a lot of commentators on the financial markets will be forecasting a crash for September-October 2016. If/when the crash happens, remember that you read about it here first and be ready to pay a much higher price (higher than zero, that is) for my next big prediction.