It’s likely that by the middle of the next decade, most new cars, trucks and buses will be Electric Vehicles (EVs). As a consequence, it’s a good bet that over the next several years the demand for both gasoline and diesel will shrink dramatically while the demand for electricity (to recharge EV batteries) experiences huge growth. Part of this demand growth will be satisfied by nuclear power, which is why uranium is an indirect play on the EV trend.

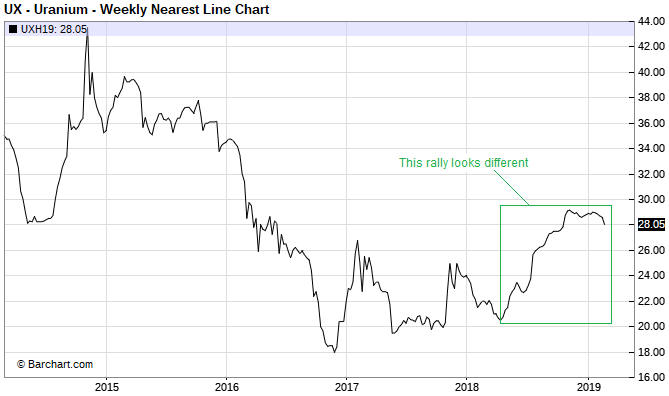

The uranium price might have begun to discount the aforementioned shift in demand in that it has been quietly trending upward since around April of last year (a weekly chart is displayed below). I say “quietly” because the rally has been accompanied by very little in the way of speculative enthusiasm. On the contrary, the rally that began last April has been accompanied by widespread scepticism.

This is an important sentiment change. Whereas every multi-month up-move in the uranium price prior to last year was greeted as if it heralded the beginning of a bull market, almost everyone has dismissed the most recent rally as just another counter-trend bounce. Being bearish on uranium has become easy, but bull markets begin when it’s easy to be bearish.

I’m not convinced that a uranium bull market is underway, but I do think that for the uranium-mining sector the intermediate-term risk/reward is skewed decisively towards reward. The reason is that the mining stocks could achieve large price gains with or without a genuine bull market in the underlying commodity. All it would take, I think, is a move by the uranium price into the $30s to convince many speculators that a major trend reversal had occurred and prompt aggressive buying of uranium-mining equities.

It used to be that owning shares of the Global X Uranium Fund (URA) was the simplest and surest way of participating in a uranium-mining rally, but that is no longer the case due to the changes that were made to this fund last year. As outlined HERE, during the second quarter of last year the index that URA tracks was changed from the Solactive Global Uranium Total Return Index to the Solactive Global Uranium & Nuclear Components Total Return Index. Thanks to this change, seven of URA’s current top ten holdings have no correlation with the uranium price.

Nowadays, owning the shares of Cameco (CCJ) is the surest way of participating in a uranium-mining rally.

It looks to me like CCJ is not far from completing a 3-year base (see chart below). I like the idea of gradually building up a position on weakness while the basing process continues.