December 3, 2019

The following charts relate to an update on the markets that was just emailed to TSI subscribers.

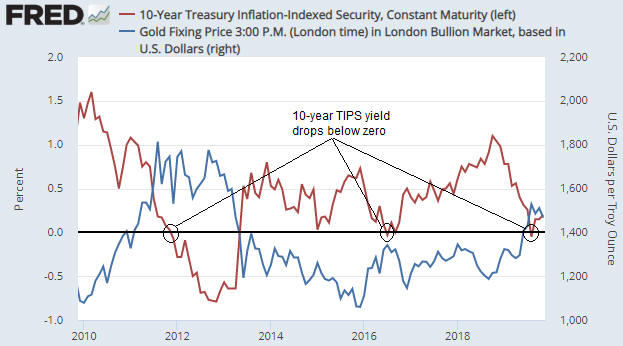

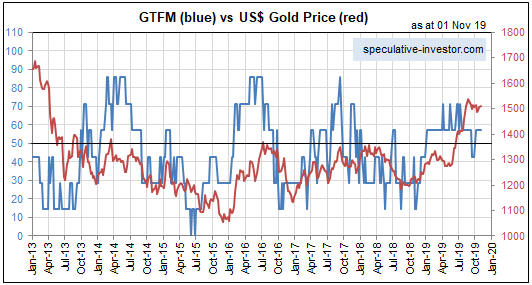

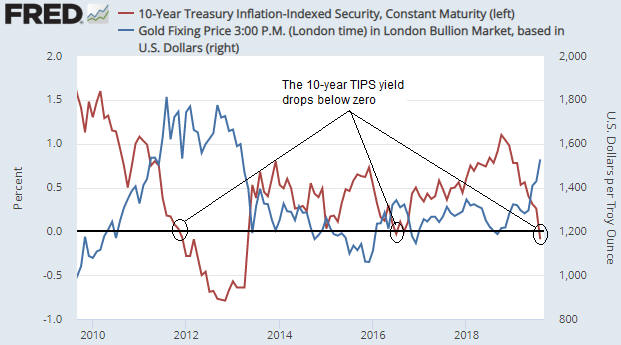

1) Gold

2) The Gold Miners ETF (GDX)

3) The Yen

4) The S&P500 Index (SPX)

5) The Russell2000 ETF (IWM)

6) The Dow Transportation Average (TRAN)

7) The iShares 20+ Year Treasury ETF (TLT)

Print This Post

Print This Post