Bank reserves are a throwback to a time when the amount of receipts for money (gold) that could be issued by a bank was limited by the amount of money (gold) the bank held in reserve. Under the current monetary system bank reserves have no real meaning, since it isn’t possible for a dollar in a bank deposit to be genuinely backed by a dollar held somewhere else. The dollar can’t back itself! However, it is still important to understand what today’s bank reserves are/aren’t and how changes in the reserves quantity are linked to changes in the economy-wide money supply. Remarkably, these bank-reserve basics are misunderstood by almost everyone who comments on the topic.

The simplest way for me to deal with the common misunderstandings about bank reserves is in point form, so that’s how I’ll do it. Here goes:

1) Bank reserves aren’t money, that is, they are not considered to be general media of exchange and are not counted in the True Money Supply (TMS). Instead, they provide ‘backing’ for part of the money supply.

2) A corollary of the above is that banks can’t use their reserves to buy things outside the Federal Reserve system.

3) Banks can lend their reserves to other banks, but the banking industry as a whole cannot expand or shrink its reserves. In other words, the banking industry has no control over its collective reserves. The central bank has total control.

4) Bank reserves can be shifted around within accounts at the Fed, but the only way that reserves can leave the Fed and enter the economy is via the withdrawal, by the public, of physical currency from banks. For example, when $100 is withdrawn from an ATM, $100 is converted from deposit currency to physical currency. This doesn’t alter the money supply, but it causes the bank to lose a $100 liability (the bank customer’s deposit) and a $100 asset (the physical currency held in the bank’s vault). When the quantity of physical currency held in a bank’s vault gets too small, the bank will replenish its supply by withdrawing reserves from the Fed in the form of new paper dollars. Although it may appear that this imposes some sort of limit on the supply of physical dollars, the Fed stands ready, willing and able to meet any increase in demand. This is further discussed in point 5).

5) Under the current monetary system, reserves effectively are created out of nothing. To be more precise, the Fed creates reserves when it purchases bonds and other assets. Since there is no limit to the dollar value of assets that can be purchased by the Fed, the banking system will never run short of the reserves it needs to meet the public’s demand for physical currency. Also, the Fed can remove reserves whenever it wants by selling bonds and other assets.

6) Except for the siphoning of reserves in response to the public’s increasing demand for physical currency, it is accurate to say that reserves at the Fed stay at the Fed until they are removed by the Fed. A corollary — as already mentioned in point 3) — is that the commercial banking industry cannot draw-down its reserves.

7) The Fed pays interest on ALL reserves, not just so-called “excess reserves”. In any case and as outlined below, for all intents and purposes all US bank reserves, with the exception of the relatively small portion required to meet any increase in the demand for physical currency, are now excess and have been for the past few decades.

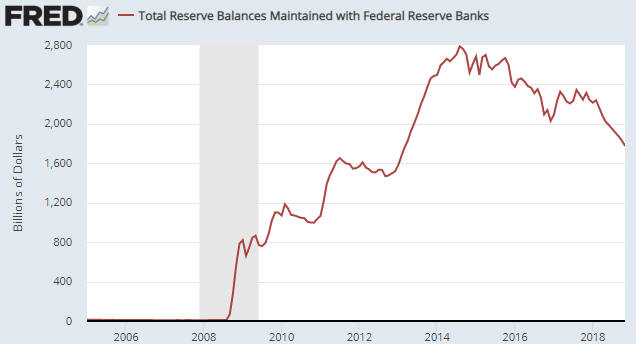

8) The way the US monetary system now works it is fair to say that all reserves are excess. The reason is that the quantity of bank reserves has no bearing on the amount by which banks expand/contract credit. In effect, the US now has a zero-reserve fractional reserve banking system. That’s why it was possible for the greatest expansion of bank credit in modern US history, which took place during 1990-2007, to happen while the commercial banking industry had almost no reserves. During this period total bank credit rose by $6 trillion, from $2.5T to $8.5T, while bank reserves at the Fed dwindled from $64B to $40B.

9) Further to point 8), bank lending doesn’t ‘piggy-back’ on bank reserves. It possibly did 40 years ago, but it hasn’t for at least the past 25 years. Hopefully, economics textbooks eventually will be updated to reflect this reality.

10) An implication of points 7) and 8) is that interest payments on reserves are neither an incentive nor a disincentive to bank lending. When a bank makes a loan to a customer it doesn’t lose any reserves and therefore continues to collect the same interest-on-reserves payment from the Fed.

11) The sole purpose of paying interest on reserves is to enable the Fed to hike the Fed Funds Rate during a period when the banks are inundated with reserves, without having to massively reduce the quantity of reserves. This was discussed in previous blog posts, for example HERE.

12) When the Fed was ‘quantitatively easing’ many pundits wrote that it was adding to bank reserves but not the money supply. This is wrong. When the Fed buys X$ of securities as part of a QE program it adds X$ to bank reserves AND it adds X$ to the economy-wide money supply. I previously described the process HERE.

13) By the same token, now that the Fed is ‘quantitatively tightening’ it is not just removing bank reserves. When the Fed sells X$ of securities as part of what it refers to as its balance-sheet normalisation program it removes X$ from bank reserves AND it removes X$ from the economy-wide money supply. In essence, it’s the process I described in the above-linked post (point 12) in reverse. That’s why the balance-sheet normalisation program is vastly more important, as far as monetary conditions are concerned, than the rate-hiking program.