An increase in the amount of gold bullion held by GLD (the SPDR Gold Shares) and other bullion ETFs does not cause the gold price to rise. The cause-effect works the other way around and in any case the amount of gold that moves in/out of the ETFs is always trivial compared to the metal’s total trading volume. However, it is reasonable to view the change in GLD’s gold inventory as a sentiment indicator.

Ironically, an increase in the amount of physical gold held by GLD and the other gold ETFs is indicative of increasing speculative demand for “paper gold”, not physical gold. As I’ve explained in the past (for example, HERE), physical gold only ever gets added to GLD’s inventory when the price of a GLD share (a form of “paper gold”) outperforms the price of gold bullion. It happens as a result of an arbitrage trade that has the effect of bringing GLD’s market price back into line with its net asset value (NAV). Furthermore, the greater the demand for paper claims to gold (in the form of ETF shares) relative to physical gold, the greater the quantity of physical gold that gets added to GLD’s inventory to keep the GLD price in line with its NAV.

Speculators in GLD shares and other forms of “paper gold” (most notably gold futures) tend to become increasingly optimistic as the price rises and increasingly pessimistic as the price declines. That’s the explanation for the positive correlation between the gold price and GLD’s physical gold inventory illustrated by the following chart.

Now, speculation in “paper gold” is both an effect of the gold price and an important short-term driver of the gold price. It is therefore fair to say that although changes in GLD’s gold inventory don’t cause anything, they often reflect changes in speculative sentiment that at least on a short-term basis do have a significant influence on the gold price. At the same time it is also fair to say that the influence of speculative buying/selling in the futures market is vastly greater (probably at least an order of magnitude greater) than the influence of speculative buying/selling of GLD shares. Refer to “The scale of the gold market” for details on relative size an influence.

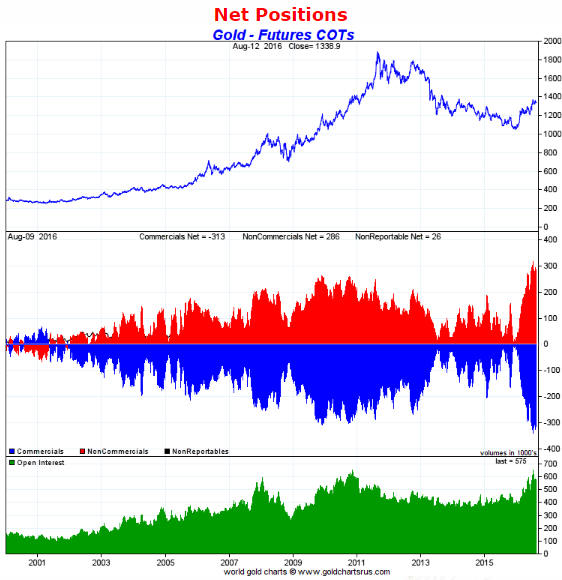

The speculative demand for “paper gold” has certainly ramped up over the past several months. This is partly reflected by the increase in the GLD inventory shown on the above chart, but it is primarily reflected by the rise to an all-time high in futures-related speculation. This is illustrated below.

Chart source: http://www.goldchartsrus.com/

The extent to which short-term speculators are bullish on gold is a risk. An unusually-elevated level of speculative enthusiasm will never be the cause of a reversal in the price trend from up to down, but it will exacerbate the decline that happens after the price-trend reverses for some other reason.