[This blog post is an excerpt from a commentary posted at https://speculative-investor.com/ last week]

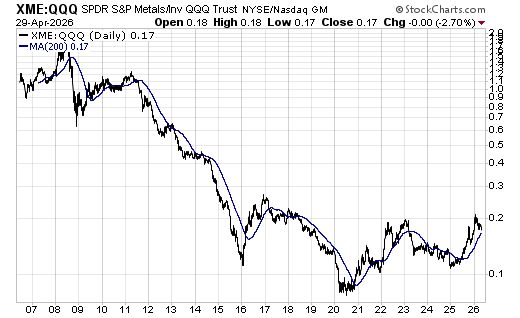

Despite all the AI hype, general mining stocks as represented by XME have massively outperformed the tech-heavy NASDAQ100 ETF (QQQ) since late-2024. In fact, the first of the following daily charts shows that XME approximately doubled relative to QQQ from its December-2024 low to its January-2026 high, while the second chart covers a longer period and puts XME’s recent relative strength into perspective. The message of the longer-term chart is that the rally in the XME/QQQ ratio from its December-2024 low potentially is the final part of a major base that began to form in 2020. This interpretation suggests that XME could double again relative to QQQ over the coming 1-2 years.

The above interpretation of the long-term chart pattern makes sense, for these four reasons:

First, the monetary inflation moonshot of 2020-2021, the trend towards on-shoring prompted by security-of-supply concerns and the long-term acceleration in government spending set in motion by the COVID lockdowns has created an economic backdrop that should continue to favour the producers of physical commodities.

Second, the companies that supply the materials needed to construct the physical AI infrastructure stand to benefit more than most software creators from the AI boom. This is because for these companies (the suppliers of the materials) the barriers to entry are relatively high and, due to physical limitations and regulations, it usually takes a long time to increase supply in response to growth in demand. During the time between growth in demand and supply catching up, there tend to be large gains in prices and profit margins.

Third, three of the past four cyclical upswings in the XME/QQQ ratio have lasted at least 2.5 years, suggesting that the current upswing won’t end any sooner than mid-2027.

Fourth, the upward trend in the breadth and intensity of military conflict that began in 2022 is bullish for inflation and commodities.

The upshot is that the decline in the XME/QQQ ratio from its January-2026 peak probably is just a correction within a major upward trend that will continue for at least another 12 months.