The events of the past 10 years have fostered the belief that central banks can create a virtually unlimited amount of money without significant adverse consequences for the purchasing power of money. Since the law of supply and demand applies to money similarly to how it applies to every other economic good, this belief is wrong. However, the ‘failure’ of QE programs to bring about high levels of what most people think of as inflation has generated a false sense of security.

The difference between money and every other economic good is that money is on one side of almost every economic transaction. Consequently, there is no single number that can accurately represent the price (purchasing power) of money, meaning that even the most honest and rigorous attempt to calculate the “general price level” will fail. This doesn’t imply that changes in the supply of money have no effect on money purchasing power, but it does imply that the effects of changes in the money supply can’t be explained or understood via a simple equation.

Further to the above, the Quantity Theory of Money (QTM) is not a valid theory. Ludwig von Mises thoroughly debunked this theory a hundred years ago and I summarised its basic flaws in a blog post two years ago. Unfortunately, QTM’s obvious inability to explain how the world works has strengthened the belief that an increase in the supply of money has no significant adverse effect on the price of money.

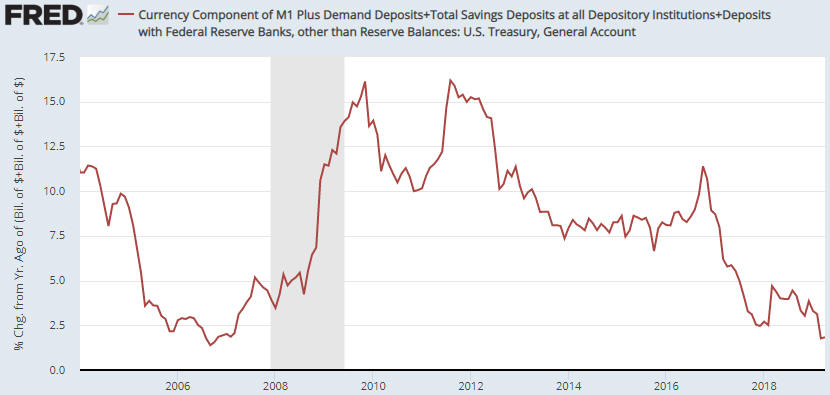

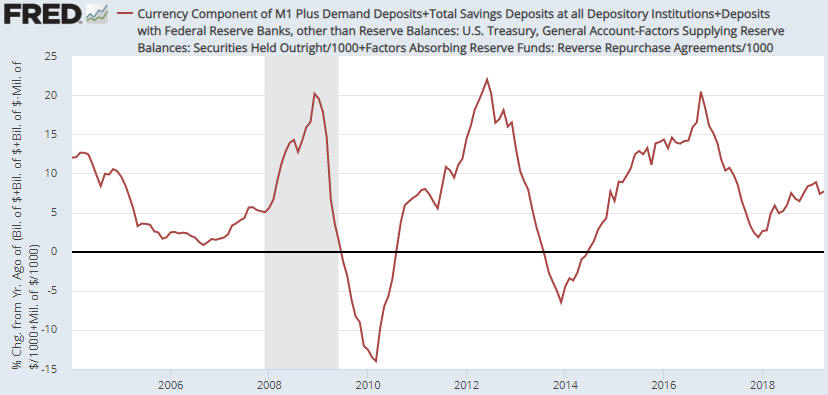

The relationship between an increase in the money supply and its economic effects is complicated by the fact that the effects will differ depending on how and where the new money is added. Of particular relevance, the economic effects of a money-supply increase driven by commercial banks making loans to their customers will be very different from the economic effects of a money-supply increase driven by central banks monetising assets. In the former case the first receivers of the new money will be within the general public, for example, house buyers/sellers and the owners of businesses, whereas in the latter case the first receivers of the new money will be bond speculators (Primary Dealers in the US). Putting it another way, “Main Street” is the first receiver of the new money in the former case and “Wall Street” is the first receiver of the new money in the latter case. This alone goes a long way towards explaining why the QE programs of Q4-2008 onward had a much greater effect on financial asset prices than on the prices that get added together to form the Consumer Price Index (CPI).

Clearly, the QE programs implemented over the past 11 years had huge inflationary effects, just not the effects that many people expected.

A proper analysis of the effects of the QE programs has not been done by central bankers and the most influential economists. As a result, there is now the false sense of security mentioned above. It is now generally believed that substantially increasing the money supply does not lead to problematic “inflation”, which, in turn, lends credibility to monetary quackery such as MMT (Modern Monetary Theory).

Due to the combination of the false belief that large increases in the supply of money have only a minor effect on the purchasing power of money and the equally false belief that the economy would benefit from a bit more “price inflation”, it’s a good bet that central banks and governments will devise ways to inject a lot more money into the economy in reaction to future economic weakness. As is always so, the effects of this money creation will be determined by how and where the new money is added. If the money is added via another QE program then the main effects of the money-pumping again will be seen in the financial markets, at least initially, but if the central bank begins to monetise government debt directly* then the “inflationary” effects in the real economy could be dramatic.

The difference between the direct and the indirect central-bank monetising of government debt is largely psychological, but it is important nonetheless. When the central bank monetises government debt indirectly, that is, via intermediaries such as Primary Dealers, it is perceived to be conducting monetary policy (manipulating interest rates, that is). However, when the central bank monetises government debt directly it is perceived to be financing the government, thus eliminating any semblance of central bank independence and potentially setting in motion a large decline in monetary confidence.

According to the book Monetary Regimes and Inflation, ALL of the great inflations of the 20th Century were preceded by central bank financing of large government deficits. Furthermore, in every case when the government deficit exceeded 40% of expenditure and the central bank was monetising the bulk of the deficit, a period of high inflation was the result. In some cases hyperinflation was the result.

In summary, growth in the money supply matters, but not in the simplistic way suggested by the Quantity Theory of Money. There’s a good chance that this fact will be rediscovered within the next few years, especially if legislative changes enable/force the Fed to monetise government debt directly.

*In the US this would entail the Fed paying for government debt securities by depositing newly-created dollars into the government’s account at the Fed. The government would then spend the new money. Currently the Fed buys government debt securities from Primary Dealers (PDs), which means that the newly-created dollars are deposited into the bank accounts of the PDs.

Print This Post

Print This Post