[This blog post is an excerpt from a recent commentary at www.speculative-investor.com]

The stock prices of companies focussed on Rare Earth Elements (REEs) rallied well in advance of the underlying commodities during May-October of last year, but recently the prices of the commodities have gone up a lot while the REE sector of the stock market has been in correction mode. This actually is normal for some commodity sectors, chief among them being REEs and lithium, during cyclical bull markets. First the equities make big up-moves while the commodities do very little, after which the equities correct/consolidate while commodity prices catch up. Then the cycle repeats, with the equities rallying anew.

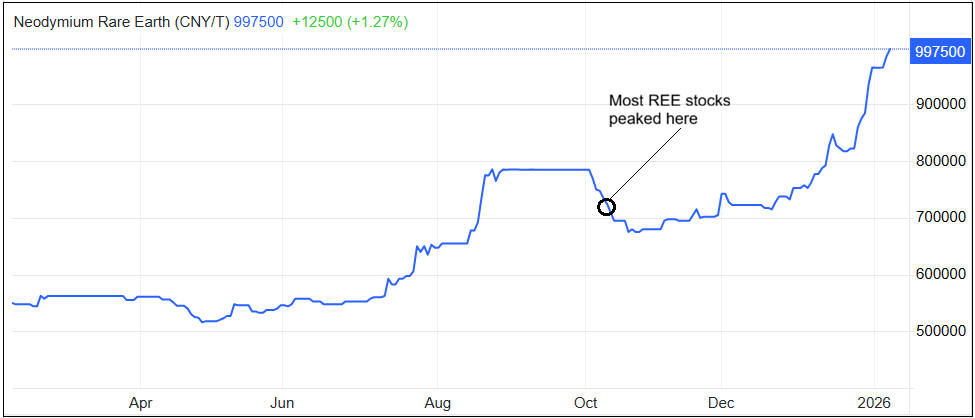

The following daily charts illustrate what we just described. The first chart shows that there was a massive rally in the stock price of MP Materials (MP), a proxy for the REE equity sector, from a low in May to a peak in October of last year, at which point a substantial correction began. The second chart shows that during May-October there was only a moderate advance in the price of Neodymium (Nd), a proxy for REEs, but that over the past two months there has been a parabolic rise to well above the October high.

Based on the historical pattern, we expect that the Nd price will level off within the coming month or so and that at around the same time the REE equities will commence new intermediate-term upward trends.

Upward pressure on the prices of many industrial commodities, including REEs, lithium, copper, tin, nickel and natural gas, will be maintained for at least another 12 months due to the on-going datacentre buildout, which not only is continuing but accelerating. Just four companies (Alphabet, Amazon, Meta and Microsoft) are together anticipating capital spending of around US$650B this year, up from the already-substantial amount of US$360B in 2025. These spending plans could explain January’s large rise in the ISM Manufacturing New Orders Index.