[This blog post is an excerpt from a commentary published last week at www.speculative-investor.com.]

In the 11th March Weekly Update we noted that the rise in the US$ gold price in the face of tight US monetary policy and high (by the standards of the past decade) real US interest rates implied concern about what’s likely to happen to the US$ in the future. We went on to write:

“At the moment this concern probably has more to do with the US government’s debt quantity spiralling out of control than the risk of the US economy entering recession in the near future. The underlying cause of concern, we suspect, is that the current administration appears to be willing to borrow/spend with complete abandon in its efforts to retain power, and there is no evidence that limiting the pace of government debt expansion is a priority on the other side of the political aisle.”

As an example of what was being done to boost his re-election prospects, we mentioned the $10,000 tax credit for first-time home buyers that had just been proposed by President Biden. Here are some additional examples from the past month:

1) A new rule has expanded the definition of a “Public Assistance Household”, which, in turn, expands the number of households eligible for Supplemental Security Income (SSI). The new rule will go into effect on 30th September-2024 (about one month prior to the election) and probably will increase the number of SSI recipients from 7.5M to more than 40M.

2) Government Sponsored Enterprise (GSE) Freddie Mac has put forward a proposal that would enable it to buy second lien mortgages. As explained in the article posted HERE:

“The aim is for Freddie to start buying fixed-rate second liens potentially by this summer, giving borrowers a way to tap an estimated $32 trillion of equity built up in U.S. homes in recent years. If approved, it would open the door for more borrowers to extract cash from their homes, without having to refinance at current 30-year fixed mortgage rates of about 7.2%.”

If Freddie Mac’s proposal goes ahead it could inject as much as $850B into the economy. If Fannie Mae, another GSE operating in the US home mortgage market, were to follow suit then the total amount injected could be close to $2 trillion. Therefore, this is potentially a very big deal.

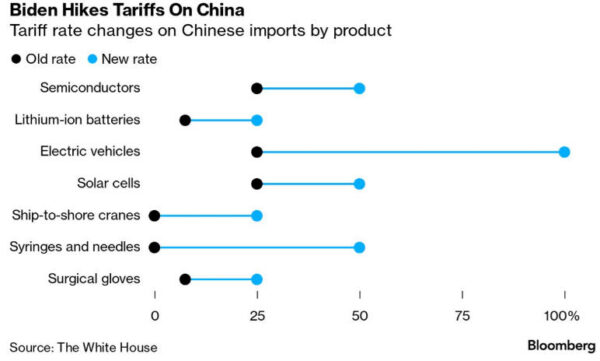

3) Earlier this week President Biden announced large tariff increases on products imported from China. The tariff hikes, which include an increase from 27.5% to 102.5% (!!) on the tariff applied to China-made Electric Vehicles (EVs), are illustrated by the following graph from the Bloomberg article posted HERE.

Tariffs are paid by the buyers (ultimately US consumers in this case), not the sellers, so the main effect of this week’s tariff increases will be higher prices in the US for some products, especially products associated with the so-called “energy transition”. The hope, of course, is that even though the economic effects of this initiative probably will be negative, the optics will prove to be favourable. In other words, the hope is that the tariff change will create the general impression that the Administration is taking actions that will help the US economy even if the opposite is true. Unfortunately, there is also a lot of support for tariffs on the other side of the US political aisle.

All of the above actions will result in the popular measures of inflation (e.g. the CPI) being higher over the next couple of years than otherwise would be the case, but if it goes ahead the one that will have the biggest effect on the financial markets in both the short-term and the long-term is opening the door for GSEs to purchase second lien mortgages. As mentioned above, this could result in almost $2 trillion being injected into the US economy. The monetary injection would occur over a period of years, but if Freddie Mac’s proposal soon gets approved then the financial world will start discounting the likely effects immediately. The effects would be bearish for the US$ and bullish for most assets and commodities priced in US dollars, including gold.

Print This Post

Print This Post