[This blog post is an excerpt from a commentary published at https://speculative-investor.com/ last week]

There is currently a major divergence within the US economy. Over the past 12 months industrial production has been flat and the ISM Manufacturing Report has been warning of imminent recession, but according to GDP calculations and forecasts the economy has grown and will continue to grow at a healthy pace (US GDP grew at a 2.1% annualised pace in Q2-2023 and is projected to have grown at a faster pace in Q3-2023). Furthermore, despite the warnings from reliable leading indicators, the dominant view now is that there will be a “soft landing” (a slowdown, but no recession). Before discussing what’s behind this divergence we’ll review the current messages from some of our favourite leading recession indicators.

First, the ISM Manufacturing New Orders Index (NOI) bounced during September-2023, but its overarching message continues to be that a recession will begin within the next few months. It would have to rise to 55 to cancel the recession warning.

Second, the following chart of the 10year-3month yield spread shows that although the US yield curve remains inverted to an extreme (the yield curve is inverted when the line on this chart is below zero), there has been a reversal from flattening/inverting to steepening. The reversal from flattening/inverting to steepening is a recession warning signal, meaning that the yield curve is now sending the same signal as the NOI.

Muddying the waters is the fact that the yield curve’s reversal has been driven by a rising long-term yield, whereas the reversal to steepening that precedes a recession usually is driven by a falling short-term yield. However, we will take the signal at face value as it is not unprecedented for the initial steepening to be caused by the long-term yield rising faster than the short-term yield.

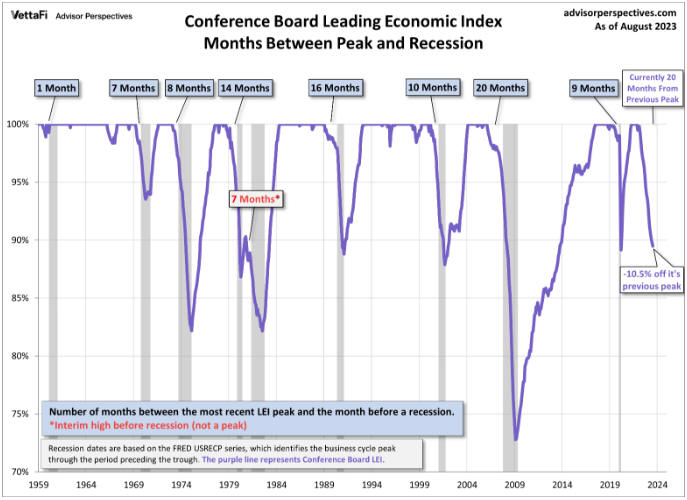

Third, here is a chart of the Conference Board’s Leading Economic Index (LEI). This chart shows that the LEI has fallen by 10.5% from its peak and that 20 months have gone by since the peak.

In the more than 60 years covered by this chart, the LEI has never suffered a peak-to-trough decline of 10.5% without the economy having entered recession and the LEI has never declined for longer than 20 months from its peak without the economy having entered recession. Assuming that the economy is not in recession today (a reasonable assumption given the coincident data), this implies that with respect to the LEI’s messaging the economy is now in uncharted territory.

The US economy is not in recession today, but taken together the above leading indicators suggest a high probability of a recession getting underway before year-end. This doesn’t mean that recessionary conditions will become obvious to most analysts and economists before year-end, though, because recession start/finish dates are determined well after the fact and because in real time the economy can appear to be doing OK during the first few months of a recession.

Returning to the question we asked in the opening paragraph, the robust economic activity still evident in some statistics, chief among them being the GDP numbers, is most likely the result of rapid government spending. This is causing the parts of the economy that are impacted the most by government spending, such as anything linked to the military or the ridiculously-named “Inflation Reduction Act”, to be strong while other parts of the economy are weak.

As an aside, due to the way GDP is calculated it can be boosted by wealth-destroying activities. For a hypothetical example, if the US government were to pay a million people $1000 each to dig a hole and then another $1000 to fill it in, 2 billion dollars would be added to US GDP. For an actual example, the on-going destruction of Ukraine is adding to US GDP because it is increasing US production of military equipment and all of the parts/materials that go into the equipment.

If the current cycle ends up being unprecedented in terms of the time from leading indicator warnings of recession to the actual start of a recession, we think that it will be due to the federal government doing aggregate-demand-boosting spending much sooner than usual during the cycle. This could delay the start of a recession to beyond the historical range, but only by creating the conditions for a government debt spiral.

Print This Post

Print This Post